What's behind the jump in global yields?

Quick note before we begin - the Trader Education Section has moved to the “Trader Wisdom” tab at the top of my homepage. Check it out, if you haven’t already.

Over the past two weeks, 10 year Treasury yields have climbed 28 bp, and have jumped 15 bp in the last two days alone. Asset prices are responding, with the S&P 500 down 2% and gold 5% from their highs. I went into this week with some risk-on positions such as long silver, BTC, and ETH, but I took profits on silver and BTC to avoid a pullback.

US economic data surprises have been coming in on the weak side, with employment, retail sales, and even inflation all coming in softer than economist surveys. I previously thought that this would translate into lower yields, but that view has been put on hold as yields have rebounded after their initial drop earlier this month. The recent jump in yields was exacerbated by three consecutive weak Treasury auctions - the 2 yr, 5 yr, and 7 yr auctions on Tuesday and Wed. Why has there been a buyers strike in Treasuries? I believe it’s for the following reasons:

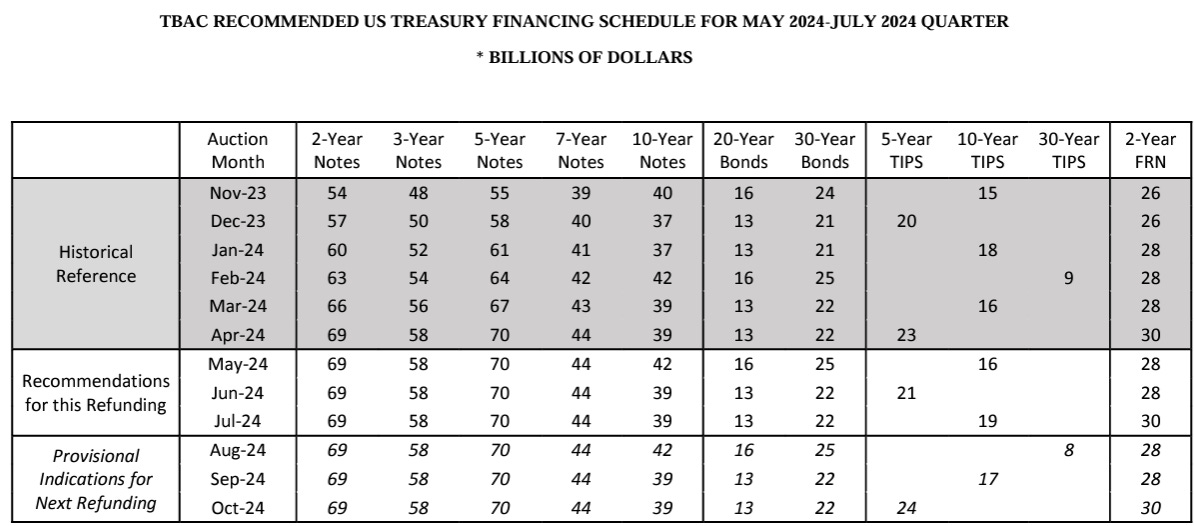

We are experiencing peak supply/demand imbalance in Treasury bond and note issuance for this year. As you can see from the table below, issuance of Treasuries is higher in May than at any point this year.

The good news is than in June, issuance of bonds and notes ticks lower (at least until August). More importantly, the Fed will reduce their monthly runoff of Treasuries by $35b in June, which means there will be $35b more in net demand for Treasuries next month.

Japanese Government Bonds have been selling off. The JGB market has been experiencing a bit of a tantrum lately, and since Japanese institutions are some of the biggest holders and purchases of global government bonds, this is affecting bond markets worldwide.

JGB 10 yr yield More importantly, 10 yr yields are now above the 1.00% level that the Bank of Japan was previously defending. Earlier this year the BoJ shifted from defending the 1% level as a line in the sand, and instead moved towards a flexible framework where they would intervene when they see fit. This creates some uncertainty around when they will step back in to support the JGB bond market. My view is that they will not let JGBs sell off in an uncontrolled manner, and will intervene within days if the pace of this selloff continues. This intervention would provide relief for global bond markets.

Inflation is still too high. Core PCE is forecast to come in at 0.3% MoM this Friday. While this is an improvement from the smoking 0.4% print that we saw in February, it doesn’t get inflation down to the Fed’s 2% target. For that reason, Fed officials are still pushing forward the message that they will keep rates where they are until they get “better confidence” that inflation is heading lower. This makes it difficult for the market to price in rate cuts, despite the weakening data. The market has been burned too many times when trying to price in rate cuts, so rallies in Treasuries and SOFR futures have been getting sold into.

How is this current backdrop different from the one that we saw in April, when SPX drew down by 7% and BTC by 23% off the highs? First, the market has moved on from worrying about geopolitical tensions between Israel and its neighboring countries, so that is no longer a bearish factor for risk assets. Second, the economic data that has come out since April has been significantly weaker, which suggests that we may see a continuation of weak data that will support the bond market at some point. The next two weeks have a high concentration of data, such as PCE inflation, ISM manufacturing and non-manufacturing, non-farm payrolls, CPI, and the FOMC. If the economy is indeed weakening, then we should see this data confirm this narrative, and Treasuries bottom out from current levels, allowing the current rally in risk assets to resume.

On to the paid subscriber section where I discuss the trades I’m putting on.

Keep reading with a 7-day free trial

Subscribe to Fidenza Macro to keep reading this post and get 7 days of free access to the full post archives.