Powell and Yellen intervene to save the day (for now)

It’s been a wild week in the markets! Japan’s Ministry of Finance intervened in usd/jpy (the Monday after I wrote about it to my paid subscribers), Yellen came out with her Quarterly Refunding Announcement (which was bearish on the surface but bullish in the details), and Powell staved off a bond market tantrum by threading the needle in his messaging.

Capital account statistics estimate that the BoJ sold $38B USD worth of usd/jpy in its intervention, which means they likely had to sell a significant amount of Treasuries to fund the selling. It’s possible that this large, price-insensitive Treasury sell flow will mark a local bottom in Treasuries, especially in light of the QRA and FOMC, both of which were dovish outcomes.

In the Treasury’s borrowing estimates released on Tuesday, they estimated a higher amount of borrowing than expected in Q2 and Q3:

During the April – June 2024 quarter, Treasury expects to borrow $243 billion in privately-held net marketable debt, assuming an end-of-June cash balance of $750 billion.[2] The borrowing estimate is $41 billion higher than announced in January 2024, largely due to lower cash receipts, partially offset by a higher beginning of quarter cash balance.

The Q3 estimate was about $100B higher than street estimates as well, as Yellen decided to withdraw an extra $100B of liquidity to run up the Treasury General Account from $750B to $850B.

The higher borrowing estimate was initially bearish for Treasuries and risk assets. However, two days later the Treasury announced that the additional borrowing would be funded entirely by bills, therefore keeping coupon issuance unchanged. Yellen is aware that issuing more bills draws funds out of the reverse repo facility (where $400B is still stubbornly sitting) and adds liquidity to the financial system.

In a well-orchestrated dance between the Fed and Treasury, Powell announced at the FOMC that they will reduce the cap on their balance sheet runoff from $60B to $25B, thus providing an incremental $35B/month of demand for Treasury coupons. This means that the dip in USD net liquidity (caused by April 15 tax payments) is in the rearview mirror and the liquidity picture should improve from here.

The highlight of yesterday’s FOMC press conference was Powell saying that current interest rates are sufficiently restrictive, and that the next move being a hike is unlikely. Prior to yesterday’s FOMC, the market had been pricing in only 30 bp of cuts in 2024, coming within shooting distance of pricing in a hike. Powell’s dovish comments capped how high the market can push short end yields, while Yellen removed the risk of a runaway melt-up in long end yields. In essence, the Fed and Treasury have put in a floor for the entire Treasury curve, which should dampen bond volatility and remove the worst fears for asset markets. The removal of downside stagflationary risks create ripe conditions for a squeeze higher in risk assets. As we look ahead to the next piece of US data in non-farm payrolls, market outcomes should be skewed towards lower yields and risk-on, as a hot number will not trigger as large of a reaction in the interest rate market as a weak number would.

Zooming out to the big picture, the federal government’s excessive spending and borrowing is unsustainable, but there are still plenty of tactics that Yellen and the Fed can use to entice the market to purchase US debt and keep the liquidity taps flowing. The Bank of Japan, for example, has been monetizing government debt for decades, but only recently has reached a point where the yen’s decline has become a concern for them. The key to trading global macro is riding the crescendos and decrescendos of the US fiscal crisis narrative within the context of the economic cycle over time.

This year’s swings in financial conditions highlight how overshoots in yields can create conditions for mean reverting moves. When Powell pivoted to a neutral bias in Dec 2023, I doubt he anticipated that the market would overshoot and price in as much as seven 25 bp cuts for 2024. Yet that is exactly what happened, causing the markets and global economic data to accelerate much faster than expected.

Now that 5 year Treasury yields (the tenor that most corporates and private equity borrow at) are back above 4.5%, economic data is undershooting expectations and recession fears are bubbling up again. The chart below of Citi’s economic surprise index shows periods shaded in green when 5 year yields were below 4.0% and periods shaded in red when 5 year yields were above 4.5%. This is evidence that current yields are restrictive, and if Powell wants to fight inflation, he doesn’t need to hike more - he only needs to deliver credible messaging that rates will be held at current levels for longer.

Even commodity prices are feeling the brunt of higher rates. The transmission of tighter financial conditions to asset prices and economic data has been pretty good this year. Readers may recall that I was bullish on commodities before the rally happened, and took profits into strength.

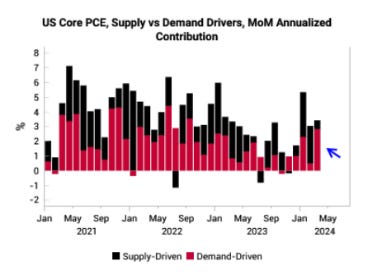

Variant Perception breaks down inflation into supply-driven inflation and demand-driven inflation. The recent jump in inflation has been driven by demand, which implies that moderating growth should lead to slowing inflation, preventing a stagflationary scare from occurring again:

The SF Fed data breaks down the drivers of inflation into demand (consumer spending) or supply and the latest data shows primarily demand driving inflation (red bars in top right chart). As long as this holds, any slowdown in growth will also drag inflation lower, reducing stagflation risks.

Thanks to the intervention of Powell and Yellen, I’m feeling more positive about risky assets as the worst of the stagflationary headwinds are behind us. Now that the market and policy makers know that the sweet spot for the economy lies in between 4.0-4.5% in 5 year yields, there is the potential to enter a goldilocks state of equilibrium. In the paid subscriber section I’ll talk about where I’m dipping my toes in the market.

Keep reading with a 7-day free trial

Subscribe to Fidenza Macro to keep reading this post and get 7 days of free access to the full post archives.