A detour into stagflation land

Risky assets have been on a nice run this year, but stagflationary storm clouds have been rolling in, signaling that we may be in for a bumpy ride ahead. In summary, we’ve seen:

Market expectations of cuts in 2024 went from 6 cuts in Jan to 1.5 cuts, back above last October’s highs.

The 10 yr Treasury has rebounded from 3.8% to 4.65%, just 35 bp away from last October’s “term premium crisis”.

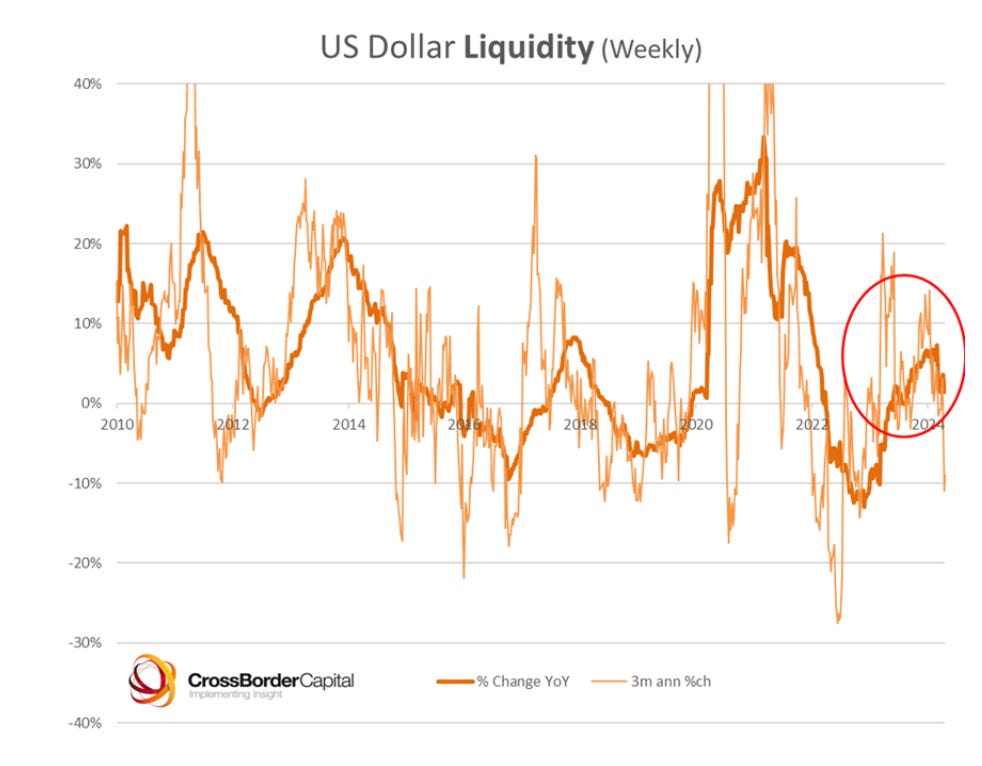

USD liquidity has turned lower due to tax receipts draining cash out of the system.

The MOVE index (an index of Treasury market implied volatility) has jumped, impairing the ability for lenders to leverage up their Treasury collateral and provide loans.

The USD index broke key resistance at 105 and is now approaching the highs from last October.

All this has been caused by inflation and growth data coming in hotter than expected, dampening expectations that the Fed will aggressively ease financial conditions this year. Up until April, equities and crypto had been trending higher, with the market believing that the strong economy can withstand the rebound in yields. However, sometime this month the market went from trading resiliently in the face of hot data to trading weakly.

Today’s backdrop looks similar to where we were last August. Last August there was a lot of optimism around AI, while yields were trending higher but hadn’t yet broken to new highs on the year. Positioning in equities was long across systematic and discretionary managers, similar to today. The Q3 QRA triggered concerns over a large supply/demand imbalance in the Treasury market, pushing yields to new highs and triggering a pullback in risk assets. Eventually the market tantrum was solved by Yellen increasing the bills to notes ratio, combined with Powell’s magical pivot towards a neutral stance. The positioning reset created the conditions for a fresh rally to new highs.

Today it is premature to expect a policy response from Yellen or Powell to support the Treasury market and risk assets. Yields haven’t yet breached last year’s highs, and equities are only 3.5% from the year’s high. The market has gone back to fearing high inflation, while the probability of the next move by the Fed being a hike has gone back up. I’m positioning for some choppy corrective action in equities and crypto for the next month, but ultimately we may see some great entry levels to accumulate longs again.

When will the Bank of Japan intervene in Usd/jpy?

Keep reading with a 7-day free trial

Subscribe to Fidenza Macro to keep reading this post and get 7 days of free access to the full post archives.