The end of American global hegemony

I’m finally back from my vacation in the US, and what a crazy two weeks it was! Trading global macro on the West Coast time zone was very disorienting. Waking up every day felt like one of those movies when you get teleported into a war zone. When I picked up my phone each morning, the market would be miles from where it was when I went to sleep. I’d have to lay in bed scrolling through the dozens of messages and emails trying to figure out what had happened overnight. Despite the less than ideal circumstances, it was one of the best runs of trading I’ve had in recent memory. I managed to capture large swathes of the epic selloffs and rebounds in SPX, the gold rally, and even the selloff in long Treasury bonds (paid subscribers can follow each trade in the Substack chat). The world as we know it might be falling apart, but at least I’m making money.

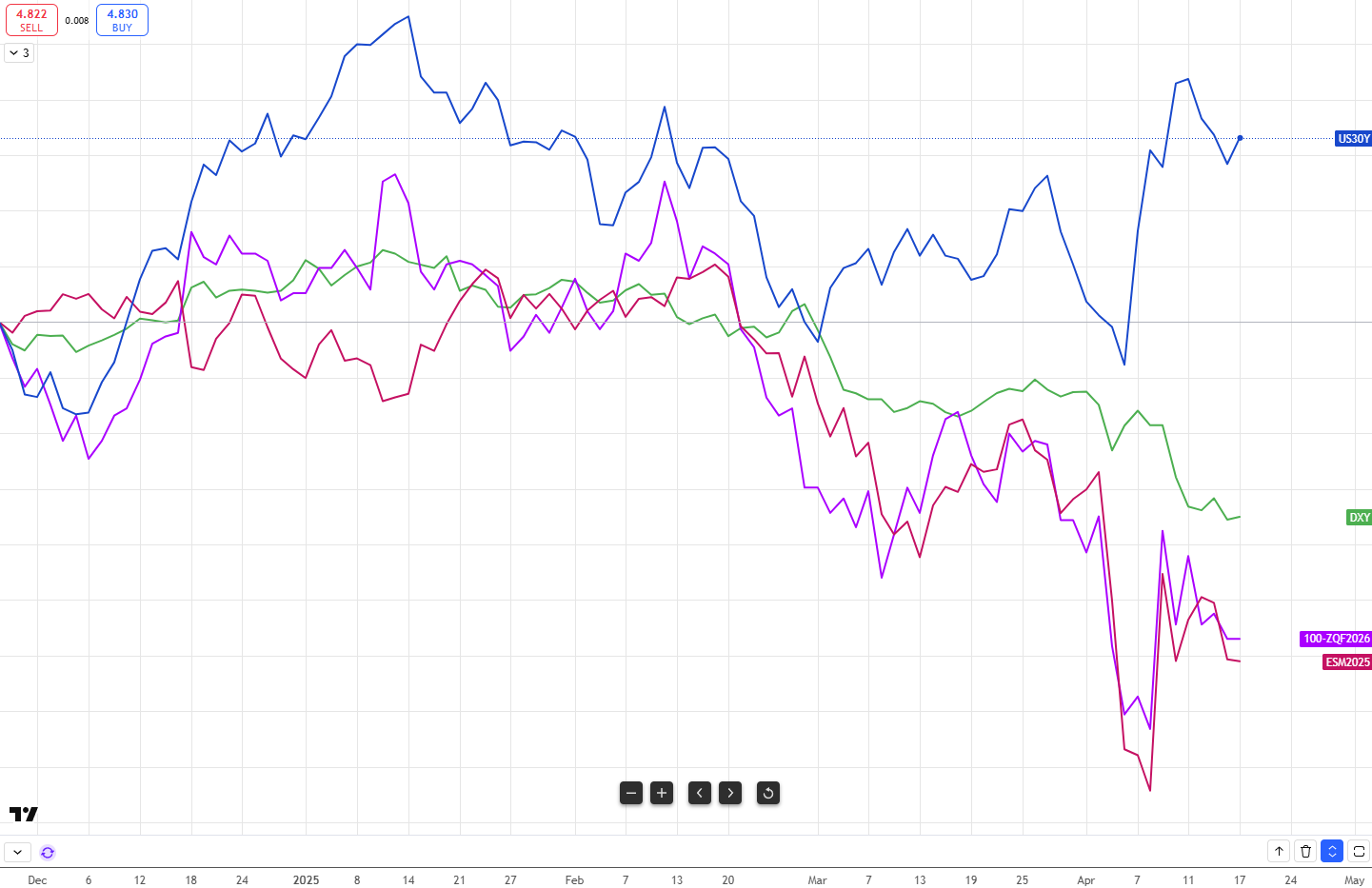

Markets have settled down as the world watches and waits for Trump to make deals with America’s trading partners. Equity markets have gyrated wildly, but what really caught my attention was the sharp selloff in long Treasury bonds and the US dollar amidst all the volatility. The following chart shows 30 yr Treasury yields (blue) surging high the week after Liberation Day while the S&P 500 (red), dollar index (green), and Fed fund pricing for the end of 2025 (purple) trended lower.

US assets are now trading like an emerging market - where the country’s stocks, bonds, and currency all fall in tandem during a crisis. Commentators have called this America’s Liz Truss moment, except instead of the UK, it’s happening to the world’s largest economy and dollar reserve currency. Global macro watchers and US fiscal hawks have been warning about the implications of America’s excessive spending and borrowing, but it was never clear when the cracks in the system would turn into fissures. Now we are seeing the first signs of the US-dominated financial system crumbling apart with the loss of the Treasury market’s safe haven status alongside a weakening of the currency.

I was sitting at a global macro lunch hosted by Gavekal this week, and one of the primary concerns of participants around the table was around why the Treasury market sold off. I believe there were three main culprits-

Foreign pension funds and institutional investors (aka “real money investors”) of sovereign debt.

Real money selling triggered the liquidation of Treasury/swap spreads and Treasury basis trades by hedge funds. These funds were long Treasuries against interest rate swaps or against Treasury futures, picking up carry while waiting for Treasuries to converge with swaps or futures. The leverage on these trades can be 10-50x, so when they go south, they have a large market impact.

Possibly China’s reserve manager selling Treasuries to punish Trump for targeting China with tariffs.

The fact that there isn’t one specific culprit you can point to is troubling, as that means this selloff wasn’t a one-off, nor can it be prevented by making a deal with a single counterparty. The markets and systematic funds are now picking up on this positive correlation between stocks and long end Treasuries, so that next time equities sell off sharply, the market will instinctively hit bids in Treasuries as well.

In addition to the exodus out of US Treasuries, foreign investors are rotating out of expensive US stocks at an alarming pace. Much of the selling over the past two months has been by foreign investors.

With both US stocks and bonds getting sold by foreign investors, it follows that the US dollar would sell off as well. I believe we are only seeing the beginning of a long term exit from US assets, which will result in a multi-year dollar bear market.

The dollar’s global reserve status - what is it good for?

The dollar didn’t become the global reserve currency out of nowhere, nor was it a natural and organic process. Its status was born out of the 1944 Bretton Woods agreement, where the Allied nations agreed to peg their currencies against the dollar and created the IMF and World Bank to cement and perpetuate this new world order. The Marshall Plan, the buildup of the American military, and America’s deal with the Saudis to price oil in dollars (creating the “petrodollar”) all contributed to the dollar’s rise over several decades following WWII. The strong US consumer helped propagate dollars to export economies around the world, while robust capital markets, strong rule of law, and the dominance of the US tech industry made America the destination for global investment capital.

In return, the US dollar and US Treasuries became a safe haven during times of global volatility. In a weakening economy, the strong dollar would help tame inflation while lower yields would ease financial conditions, laying the groundwork for a recovery. Lower yields would also allow the government to borrow cheaply and provide fiscal stimulus to support the economy during a recession. The dollar reserve currency status provided the benefit of having automatic stabilizers buffering the economy and financial markets from volatility, and the safe haven status of Treasuries meant that there was always a willing buyer for its debt. This automatic stabilizer and endless demand for Treasury bonds has been referred to as America’s “exorbitant privilege”.

Emerging markets without such exorbitant privilege find their borrowing costs and currency depreciating during times of crisis, creating a feedback loop that deepens recessions or stokes runaway inflation. Policy makers are left with hard choices - defending the currency by hiking interest rates would deepen economic weakness and depress financial markets, but letting the currency go would fan the flames of inflation and weaken the credibility of their financial system.

Why are things falling apart now, and can the US bounce back?

America’s global hegemony would have survived much longer if Trump and his predecessor Biden had made concerted efforts to bring down the budget deficit. Instead, Trump is tearing up the treaties and alliances that upheld America’s dominance, eroding investors’ faith in the judicial system, threatening the Fed’s independence, and driving allies and trading partners into the arms of China. Instead of staving off America’s decline, he is accelerating the unwind of decades of efforts by America’s statesmen and sacrifices by military servicemen to build and maintain America’s dominance.

Trump’s election platform of fiscal conservatism provided temporary hope that the US could turn its debt/GDP ratio around. Unfortunately the efforts of DOGE, Trump and Elon Musk’s program to bring down the budget deficit, is cutting spending too little and too slowly. The DOGE website estimates $155B of spending cuts in 2025 - a drop in the fiscal bucket.

With long end interest rates rising, DOGE failing to deliver meaningful cuts, and a growth slowdown looming, the US budget deficit will likely expand, not contract from its current 6.3% of GDP. The window to enact any meaningful fiscal conservative policies has closed, and long term holders of US assets are now panicking.

The path towards the endgame

The unwinding of America’s global hegemony will likely take place over years in the form of one crisis after another. Each crisis will be fixed with a bandaid that addresses the symptoms but not the underlying cause. The Fed will likely continue to cut rates, but as we saw last September, this doesn’t lead to lower yields in the long end. The Fed can change regulations around SLR exemptions to allow banks to purchase Treasuries on their balance sheet, but the timing and impact of this policy change is unknown. The Treasury can also accelerate buybacks on the long end, funded by borrowing on the short end. These policies will incrementally support demand for Treasuries but will not stem the swelling tide of issuance that continues to grow year by year.

Eventually the borrowing costs of the US will become too painful to bear, and the Fed will have no choice but to support the bond market. It may potentially take years to reach this point, but when it does, the dollar decline will accelerate. I look towards the British pound as a cautionary tale for how this long-term decline will play out. Below is a chart of what it looks like when a country’s currency loses its global reserve currency status.

Almost every investor has investments in US assets, and it is difficult to protect one’s portfolio against the unfolding exodus from US assets. However, I believe that global macro traders are well positioned to profit greatly from this watershed transition.

In my next post I will discuss what I’m calling the “American exodus complex” - several trades that I am putting on to express my views above.

Bonus content:

The prospect of America losing its global hegemony to China has led me to the conclusion that China will inevitably rise as the next global superpower. The links below discuss why this is likely, and what the world would look like if it happens.

Disclaimer: The content of this blog is provided for informational and educational purposes only and should not be construed as professional financial advice, investment recommendations, or a solicitation to buy or sell any securities or instruments. The blog is not a trade signaling service and the author strongly discourages readers from following his trades without experience and doing research on those markets. The author of this blog is not a registered investment advisor or financial planner. The information presented on this blog is based on personal research and experience, and should not be considered as personalized investment advice. Any investment or trading decisions you make based on the content of this blog are at your own risk. Past performance is not indicative of future results. All investments carry the risk of loss, and there is no guarantee that any trade or strategy discussed in this blog will be profitable or suitable for your specific situation. The author of this blog disclaims any and all liability relating to any actions taken or not taken based on the content of this blog. The author of this blog is not responsible for any losses, damages, or liabilities that may arise from the use or misuse of the information provided.

I agree with you, and the loss of potential for continued positive American influences gives me melancholy.

Great post, thank you for educating. Would love to hear more in your next post if and how an accelerating world will influence the rate of USD decline. GBP played out over many decades and the market seems much faster and more reflexive nowadays.