Liquidity drain starts today - what will the market impact be?

With the debt ceiling passed, the widely discussed refill of the Treasury General Account starts today. The Treasury is selling $173B of Tbills and is scheduled to sell more on Wed and Thurs (amounts not yet announced). What’s interesting is that different asset classes - equities, Treasuries, and crypto - are positioned going into this period in vastly different ways.

The bond market has been the most aggressive in pricing in the large supply of issuance, pushing Sept 2023 SOFR rates to the highest levels since SVB blew up.

Meanwhile, record shorts have built up in 2 yr Treasury futures. A portion of Treasury shorts are from basis trades (hedge funds buying cash and short futures, waiting for them to converge), but a lot of the positioning is directional as well. This is because excessive positioning can be seen in every part of the Treasury and SOFR curve, not just in the areas where funds have put on the basis trade. My view is that changes in economic fundamentals do not justify the magnitude of the move in yields and the size of the short positions, and therefore they are mostly explained by anticipation of Treasury issuance.

Meanwhile, equities are on an AI and FOMO driven rampage, as retail and institutional buyers have been scrambling to re-up their equity allocations. The S&P 500 is clearly not concerned about the drain of liquidity that will happen as a result of outsized Tbill issuance.

Consolidated equity positioning from Deutsche Bank shows that the market is now close to neutral.

Meanwhile, the put-call ratio suggests excessive bullishness or complacency

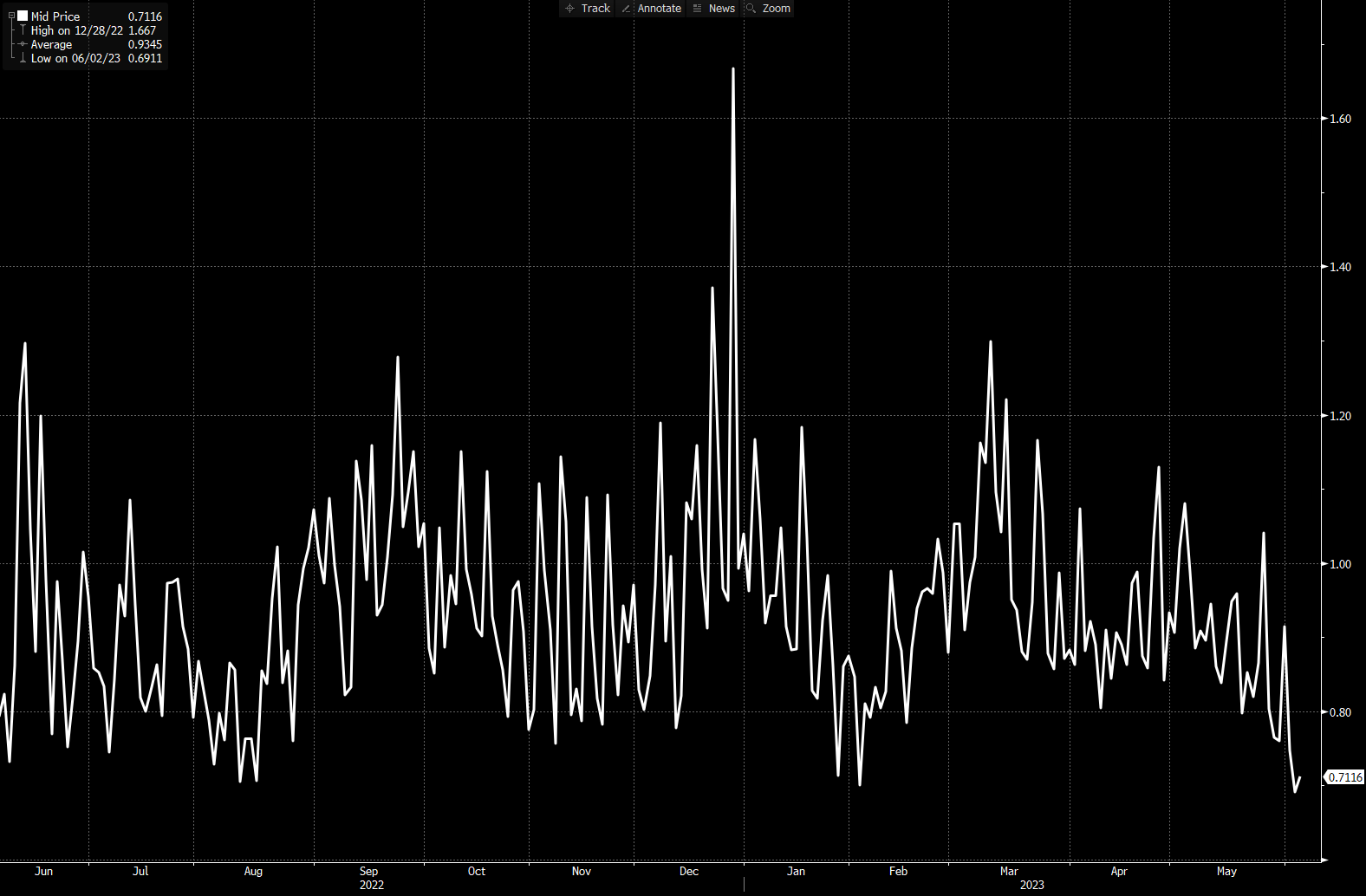

The VIX is back at lows not seen since the QE-fueled bull market of 2021

Could equities be right, or are they mispriced? In the paid subscriber section, I’ll address the arguments for why the Tbill issuance is not bearish for equities. I’ll also dig into what happened to equities and crypto the last time there was a large drop in net liquidity. Finally, I’ll share how I’m looking to position myself on day one of the liquidity drain.

Keep reading with a 7-day free trial

Subscribe to Fidenza Macro to keep reading this post and get 7 days of free access to the full post archives.